There is no common understanding yet of the future direction of the global economy. There are several different points of view about it. The growth of inflation will sooner or later make central banks curtail their monetary stimulus program, which will definitely affect the quotes. Let’s look into the situation and talk about the short-term future of the global financial markets.

The views expressed by different analytical agencies and independent experts can be boiled down to the following possible scenarios for the financial markets in the next couple of years:

- Apocalypse: the markets will soon end up in a drawdown. For the US markets, it will mean a 40% or 50% drawdown, the same way the Dow Jones Industrial Average was losing its value during the stock market downturn of the 2000s and the financial crisis of 2007-2008.

- Gradual drawdown: the key indices will gradually lose from 20% to 30% and resume their growth.

- Optimistic scenario: the markets will continue growing without any significant correction.

Each of these points of view is backed by solid arguments both for and against. In this article, we will discuss them in detail and try to find out why the first two scenarios are more likely to happen than the third one.

Scenario 1. Apocalypse

Prerequisites for a further deep correction are already in the air. This correction could reduce the value of the indices of developed countries by 40-50%. The indices of developing countries, traditionally, will lose up to 80% in value. Why can this happen? Everything is quite simple: this scenario may come true if central banks of developed countries refuse to take the further economic support measures necessary during the pandemic.

George Cooper, an economist, has done an excellent job of showing how economies are regulated in his book “The Origin of Financial Crises.” In this book, he described the process using a Eurofighter Typhoon as an example. The Eurofighter Typhoon is a combat aircraft with an intentionally aerodynamically unstable design. It can reverse its flight path quickly. However, this creates certain difficulties in controlling the aircraft, and the fighter’s electronic systems are constantly adjusting its control surfaces (constantly is key here). Economic policies are constantly adjusted in the same way in order to control the “flight” of the economy.

In the crisis year of 2019, there was a significant deviation of economic processes from the norm. The pandemic disrupted the supply chains, led to reduced consumption and a significant rise in unemployment. Most central banks did the same to adjust to the situation: they started printing money. They cut the key rates and pumped money into the markets through Quantitative Easing (QE) programs.

Additional cash injections helped companies survive and prevented them from going bankrupt. The markets that could have collapsed also managed to hold on. There is a limit to everything – the inflation rate in most countries is getting higher, which means that the economic aircraft has to be adjusted, i.e., the process of injecting cheap money into the markets has to be stopped. As a consequence, the central banks must taper QE programs and raise the rate, which will lead to the following interrelated implications:

- The rise of the government bond yields.

- The stock market crash.

- The rise of the USD.

- The rise in gold prices.

As far as the stock market is concerned, companies with high debt loads and large stakes in highly leveraged companies will be hardest hit. This is why news about major corporate defaults (as happened with China’s Evergrande) will be most acutely felt.

Take the example of Evergrande. It best illustrates the levels of economic integration and the investors’ fear. In September, market participants paid attention to Evergrande, China’s largest real estate developer. The company had accumulated $305 billion in debt, but it had no money. It would seem that European markets have nothing to do with this.

First of all, everyone immediately drew an analogy with the bankruptcy of Lehman Brothers in 2008 and what it ultimately led to. The pain of the subprime mortgage crisis has not subsided yet, and Evergrande, as luck would have it, is a real estate giant. Secondly, everyone remembered that the US hedge fund BlackRock is the largest lender of the Chinese company. Evergrande owes about $400 mln to it. The Chinese property giant also owes $275 mln to the Swiss UBS Group, about $200 mln to the British HSBC, and $430 mln to the Ashmore group. Thirdly, one of the main reasons is that the markets are susceptible to negative news, which is now more of a psychological problem than an economic one.

Hence, we can conclude that the markets now will react especially sharply to literally anything. Understanding this, central banks and their heads will try to soften the blow in every possible way, which makes us think about the second possible scenario.

Scenario 2. Gradual Drawdown

Pay your attention to the central bank heads’ rhetoric. In a nutshell, this is what they say:

- Is the inflation rate increasing?

- Yes, it is.

- Is the unemployment rate declining?

- Yes, it is.

- Is it time we stopped injecting liquidity?

- It’s hard to say. Maybe it is.

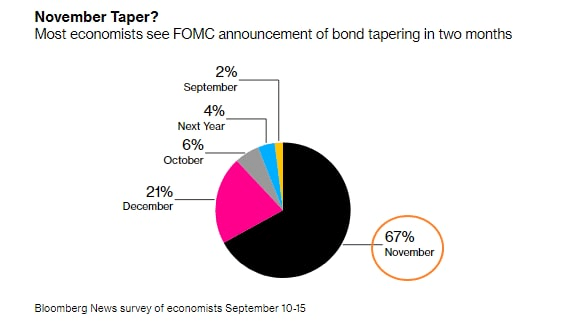

There is no definite answer to the question of when the tapering starts and the transition to a tighter policy begins. We can, however, say with certainty that the rhetoric of the monetary authorities is gradually becoming restrictive.

Analytical agencies used to make predictions about the tightening of monetary policy in the long term. Today, more and more experts say that tightening will begin in the next six months to a year. According to the surveys conducted by CNBC, BBG, and RTRS, the Fed will already hint at the beginning of reining in its emergency stimulus measures at the November meeting.

This is how the Fed and other central banks are trying to set up a gradual drawdown of the markets, which can be called a “technical correction” of 20-25 percent. Such a correction would solve two key problems:

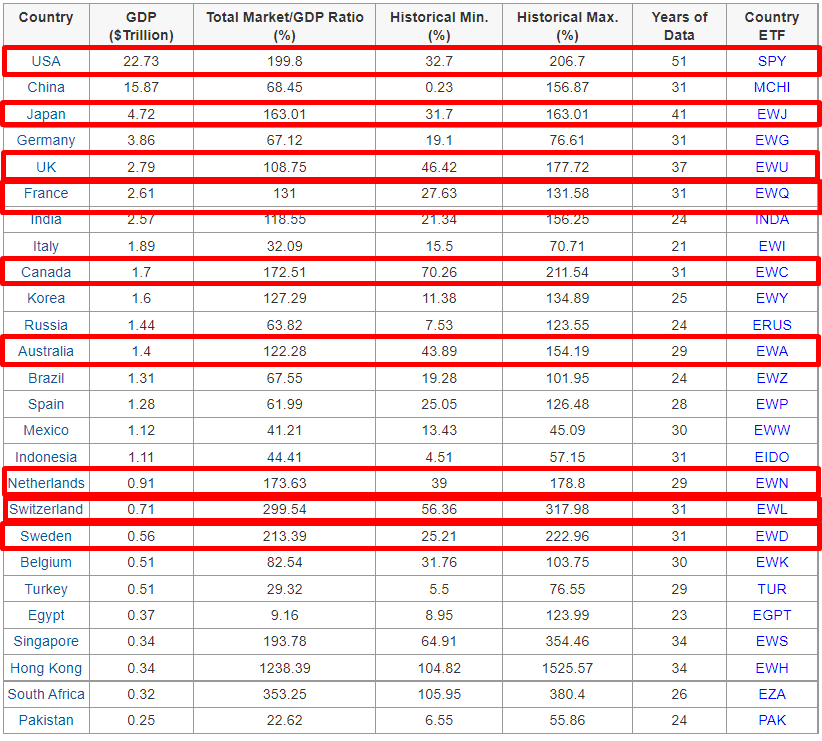

- It can help reduce the market overheating — at the end of the first half of the year, the US GDP capital-output ratio (the ratio of market capitalization to nominal GDP) is about 200%. A similar situation is observed in all the other developed economies.

- Maintain consumption. Remember that about 60% of the US households are members of the 401(K) program. That is to say, they are investing in the stock market through a retirement plan. Thus, a repetition of the year 2008 scenario is not the best option for the Fed.

The drawdown should be as smooth as possible, and the ideal option would be to do without it altogether.

Scenario 3. Optimistic View

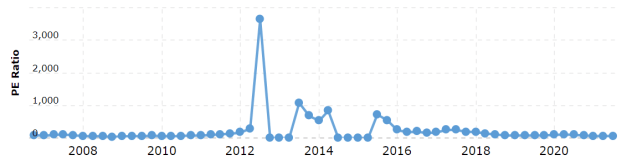

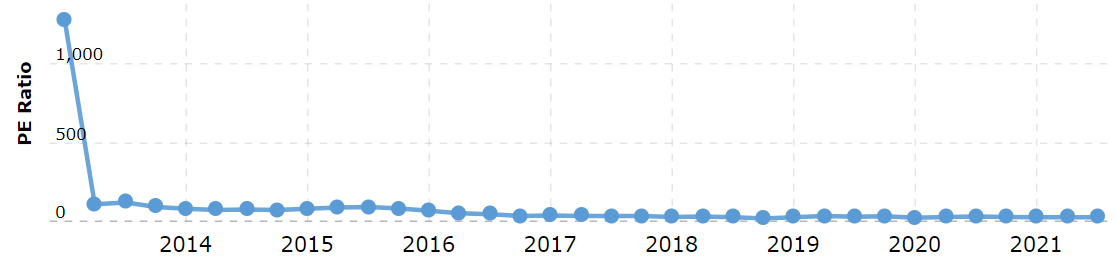

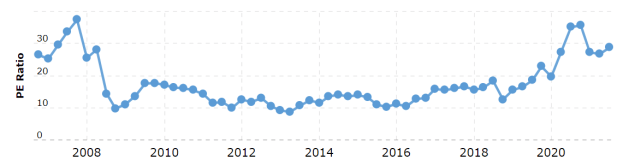

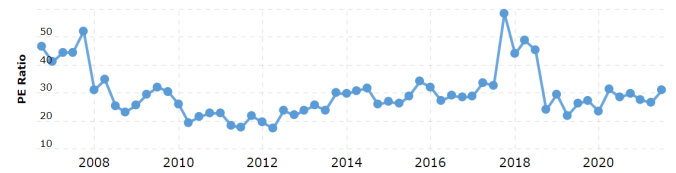

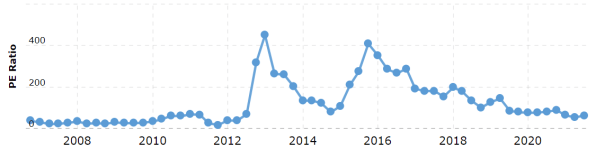

Supporters of this scenario also have their own rather weighty arguments. Let’s take a look at the situation with the FAANG stock. The average P/E ratio of Facebook, Apple, Amazon, Netflix, and Google is 41.46, which means that the payback period for these securities exceeds 40 years on average. However, the interesting point is that the P/E ratios of almost all these companies have remained relatively high over the last five years.

As you can see, only Apple’s P/E is close to its extreme values. Other US giants have no such problem.

It confirms the rule that there is nothing special about growth companies’ key stock multiplier P/E ratio being quite high. As a consequence, supporters of the optimistic scenario point out that market overheating is nothing but a myth. Moreover, there is an opinion that large market participants intentionally create a negative external background in order to add “cheap” shares to their portfolios.

Conclusion

All three scenarios have a right to exist, and it’s up to you to decide which one you should make use of. Common sense says the first and second scenarios are more likely to occur because a crisis is always a time of opportunity, and a deep crisis (scenario 1) is a time of great opportunity.

A stock market drop of 40-50% would provide an opportunity to add cheaper securities to your portfolio and make a decent profit once the restrictive monetary cycle is over. The only important thing is to have cash on hand when you might need it. The Olymp Trade platform offers its Stock Price Trade mode to those who would like to invest in cheap securities without paying fees for opening a position.